FINANCIAL ADVICE CENTRE NEWS

Your Spring Newsletter 2019

Your Adviser Discusses

Inheritance Tax (IHT) and the Investment Options

We discussed IHT in our inaugural newsletter in 2017, but as it is a topic clients are often asking for advice or reassurance in, we thought we would provide you with a fresh update and reminder about allowances.

Inheritance tax facts: what is IHT and who does it affect?

Inheritance tax is a tax payable on the assets (money or possessions) you leave behind when you die, so it’s often referred to as ‘death duty’.

The assets making up your estate can include:

- Cash and savings in the bank

- Investments

- Property and valuables, such as art, jewellery etc.

- Vehicles

- Businesses you own

- Pay-outs from life insurance policies not held in trust

If you make certain kinds of gifts during your lifetime, but die within seven years after making them, the recipients of the gifts may be liable to pay IHT.

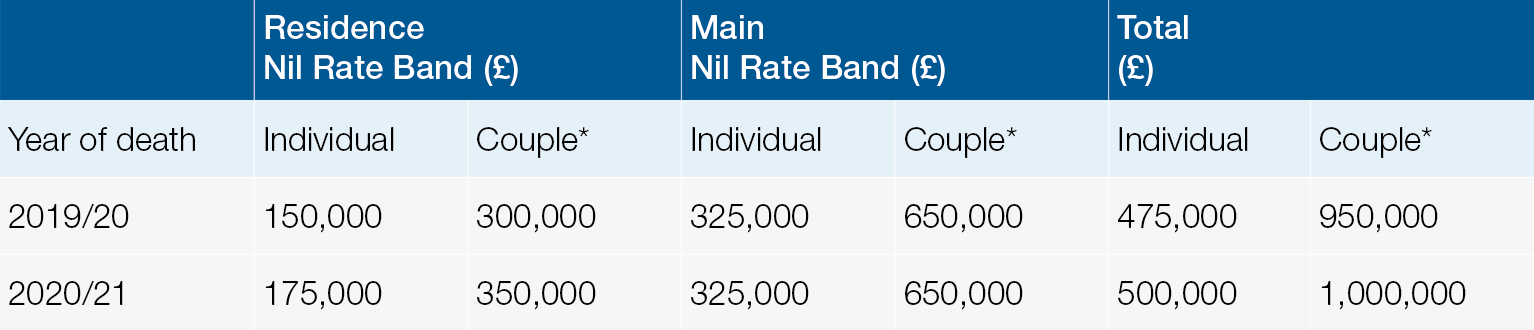

The Residence Nil-Rate Band (RNRB) allowance, that was introduced in April 2017, is now at £150,000 for each individual which gives a current allowance of £475,000 for the majority of us with total assets under £2 million.

From April 2020 this will increase to £175,000 per person and then increase with CPI each year thereafter. There is no plan at this time to link the Nil Rate Band with CPI so we can see this remaining at £325,000 for the foreseeable future.

* Couple in this context means individuals that are legally married or in a registered civil partnership

The reiterate RNRB is fully available to anyone who:

- passes the family home to ‘direct descendants’ - broadly their children/grandchildren and/or their spouses on death; or

- had a family home, then downsized on or after 8 July 2015 (passing on assets of equivalent value to children/grandchildren); and

- has an estate below £2M.

What are my options when it comes to managing IHT?

Of course, there are ways that you can legitimately reduce or even fully mitigate the impact of IHT such as spending it, or setting up Life Cover to pay the tax after your death but there are also specialist investments that achieve IHT relief after just two years.

These investments are perceived as a higher-risk approach but it offers quick relief, a potential 40% saving as long as you survive two years and means you do not have to give it away if you think you may need it.

These investments are made up of investments within companies that qualify for Business Property Relief (BPR). BPR is an established form of tax relief that gives people an incentive to invest their money into trading businesses. It was introduced in 1976 as a way to ensure that inheritance tax wasn’t paid on small businesses. Shares in a BPR-qualifying business can be left to beneficiaries free from inheritance tax, provided they have been owned for at least two years at the time of death.

Different products we use to meet these rules are Enterprise Investment Schemes (EIS) and portfolios of companies listed on the Alternative Investment Market (AIM) which can be held within an ISA.

EIS was introduced in 1994 to encourage investment in new unlisted companies. The finance raised through EIS investment helps to support the UK economy as the capital is used by businesses to develop and grow. EIS offers a range of valuable tax reliefs to encourage investment and reduce inherent risks. To qualify for tax relief, investments must be held for a minimum of three years. The benefits include:

- Up to 30% Income Tax relief

- 100% Inheritance Tax (IHT) after two years (and if held at time of death)

- Capital Gains Tax (CGT) deferral relief

- Growth free of CGT

As EISs are investing in unlisted and start-up companies there is an inherent risk that some of these companies fail. We look to use investment providers who manage this risk well and use a diversified range of new companies. However, they are not risk free so seeking advice is crucial before entering into these investments.

AIM ISA’s were launched in 2013 when the Government changed the rules to allow AIM-listed shares to be held in an ISA. Some of our investment providers launched the full AIM services in 2005 so have great track records over the past 14 years. Investments within or outside of an ISA invest in shares listed on the Alternative Investment Market (AIM) that can qualify for relief from inheritance tax. These tax reliefs are part of a wider initiative to encourage people to invest in smaller companies.

The ISA’s might be good for you if:

- Your estate is likely to be liable for inheritance tax.

- You have built up significant ISA holdings over the years.

- You want to keep the lifetime tax benefits of your ISAs while reducing the inheritance tax liability for your beneficiaries.

- You are comfortable with the risks involved with investing in smaller companies.

More than 6 million of the UK’s 23 million ISA investors are over 65 years old.

Clients with significant funds invested in ISAs often face a common dilemma. On the one hand, they could keep their ISA money invested and continue to get tax-free growth and income, while recognising that when they die, their family may have to pay inheritance tax on the value of their ISAs. On the other hand, they could reduce the amount of their estate liable for inheritance tax by cashing out of their ISAs, then gift the money to their family, or move the proceeds into trust.

But making gifts or using trusts also presents problems. Not only does taking the investment outside of the ISA wrapper mean you lose the ISA tax benefits, but you also relinquish control over the assets.

What we can do is keep your assets within an ISA, maintaining all the benefits of this tax efficiency but also have them outside your estate after just two years.

With all of the AIM listed investments there are similar risks:

- Your capital is at risk

The value of your investment can go up or down and you may not get back the full amount invested. Investing in AIM-listed shares involves more risk than investing in shares of companies listed on the main market of the London Stock Exchange.

- Your investment could experience volatility

The performance of AIM-listed shares tends to be more volatile, which means their value can rise or fall by greater amounts on a day-to-day basis.

If you would like more information on these investment types of on IHT generally then please let me know and I would be more than happy to discuss this further with you.